Effective Strategies for Credit Card Debt Relief and Reduction

Most people think of credit card debt as a problem to solve with a single method, but managing debt can be more flexible and personal than that. Instead of choosing one strategy and sticking to it rigidly, it can be helpful to think of these tools as part of a larger financial toolkit. Approaching repayment this way makes it easier to adapt your plan as your life, income, and goals shift. This mindset also opens the door to exploring options such as credit card debt relief while still recognizing the value of do-it-yourself strategies that you can control from start to finish.

Your Habits Matter Most

When you take a customizable approach to debt repayment, you begin by examining your financial habits rather than your balances alone. Understanding why certain cards carry higher balances or why minimum payments feel overwhelming can guide you toward a strategy that addresses the root causes. For example, someone who is motivated by quick wins may lean toward the snowball method, while another person focused on saving interest may choose an avalanche style plan. Neither is better universally. The effectiveness depends on the individual’s preferences, consistency, and comfort level with change.

Combining methods can also create a faster path to reducing debt. A balance transfer might lower interest for a while, giving you room to apply more money toward your highest priority card. Pairing that with a structured payment method allows you to stay organized and build momentum. The key is to see your options as interconnected pieces rather than isolated solutions.

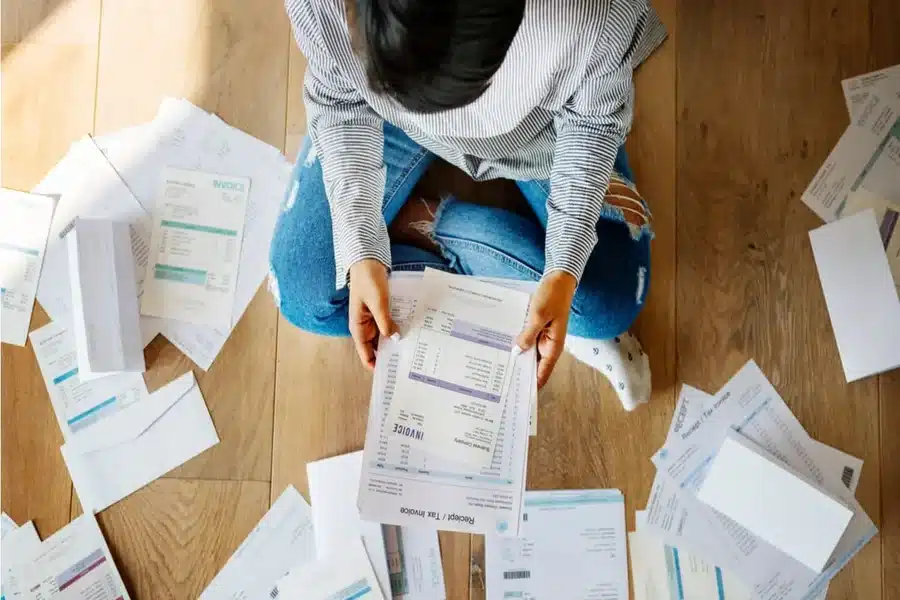

Starting with a Clear Financial Picture

Before choosing strategies, it helps to understand your full financial situation. This means looking closely at your balances, interest rates, recurring expenses, and available income. Many people find this step surprisingly eye opening because they discover patterns they had not noticed before. A few accounts may be responsible for most of the interest charges, while others feel manageable with small adjustments.

When you gather this information, it becomes easier to build a plan that fits your needs rather than forcing yourself into a generic method. You can see where a balance transfer would make sense, where payments can be increased, and which accounts can be handled later in the process without risking additional stress.

Using the Avalanche and Snowball Methods to Build Momentum

The avalanche method focuses on paying off the card with the highest interest rate first. This method reduces the total interest you pay over time and tends to be the most cost effective. However, it can feel slow because the highest interest balances are often the largest.

The snowball method targets the smallest balance first. Even though this might not save as much interest, it delivers quick wins that help maintain motivation. Many people benefit emotionally from the snowball approach because it creates visible progress early on.

Neither method needs to stand alone. You can blend the two by prioritizing a small, high interest card, then shifting to a more traditional avalanche pattern once early victories give you a morale boost.

Exploring Balance Transfers with Intention

Balance transfers can be powerful when used with a clear plan. Transferring a balance to a card with a zero-interest promotional period creates breathing room to pay down what you owe without watching interest accumulate. However, the technique works only when you commit to paying off the transferred balance before the promotional period ends.

The United States Federal Reserve provides helpful guidance on how credit card interest operates, which is essential for understanding what a balance transfer can truly save. Their resource on how credit card interest and repayment work offers useful insights for planning your strategy.

Before completing a transfer, review any fees, the length of the promotional period, and any rules related to new purchases. These details determine whether the transfer reduces your burden or simply shifts it.

Contacting Creditors for Rate Reductions or Hardship Options

Reaching out to your creditors directly can feel intimidating, but many lenders are more willing to negotiate than people assume. Calling to request a lower interest rate, a temporary payment reduction, or a hardship program can provide immediate relief and help you stay consistent with your repayment plan.

Before making the call, gather your account details and decide what you want to ask for. Knowing your numbers helps you communicate clearly and increases your chances of receiving support. Sometimes creditors can reduce your rate by several points, which meaningfully improves your progress.

Strengthening Your Budget to Support Debt Reduction

Budgeting is one of the most powerful tools you can use when reducing credit card debt. A well-structured budget assigns every dollar a purpose and strengthens your awareness of spending habits that create unnecessary financial pressure. The Consumer Financial Protection Bureau provides helpful resources on building a practical household budget that can support debt repayment without feeling restrictive.

A strong budget does not require perfection. What matters is consistency. Even small monthly increases in your debt payments reduce interest and shorten repayment timelines.

Combining Strategies for Sustainable Progress

Many people find success by combining multiple approaches. For example, you may start with a balance transfer to reduce interest. Then, once the transfer is complete, you might use the avalanche method to target the highest interest card while applying snowball principles to maintain motivation.

These combinations make debt reduction more adaptable. If your income changes, you can scale your payments up or down without abandoning your plan. If a card receives a promotional offer or you qualify for hardship relief, you can incorporate those changes seamlessly.

Staying Motivated Throughout the Journey

Debt reduction is not just a financial effort. It is an emotional one. It requires patience, self-awareness, and a willingness to adjust your plan when life shifts unexpectedly. Staying motivated often comes from celebrating progress. Paying off even a single card can create a renewed sense of confidence.

It also helps to remind yourself that the strategies you choose are not about being perfect. They are about being consistent. Over time, consistency wins every time.

Final Thoughts

Effective credit card debt relief comes from selecting strategies that match your personality, financial situation, and long-term goals. When you allow yourself to combine methods, explore new tools, and adjust as needed, you create a plan that is sustainable and empowering.

Debt does not disappear overnight, but with a thoughtful approach and a willingness to adapt, you can reduce your balances, relieve financial stress, and build a more secure future.